International insured losses from pure catastrophes hit US$137 billion in 2024, following the 5%-7% annual development fee that has been the norm in recent times, based on Swiss Re evaluation.

If this pattern continues, international insured losses will method US$145 billion in 2025, primarily pushed by secondary perils equivalent to extreme convective storms (SCS), floods and wildfires, stated the Swiss Re sigma report titled “Natural catastrophes: insured losses on trend to USD 145 billion in 2025.”

Whereas loss severity is rising globally, North America accounted for nearly 80% of worldwide insured losses in 2024, as a result of area’s publicity to extreme thunderstorms, hurricanes, floods, wildfires, and earthquakes, the report stated. (Editor’s observe: the 80% determine might be discovered on web page 29 of the primary report, desk 3).

“After a number of years of underwriting losses, owners’ premiums solely not too long ago caught up with housing alternative prices. Nonetheless, ongoing underwriting losses counsel that premiums are nonetheless not commensurate with the chance, and that additional alignment is important to maintain insurance coverage enterprise.”

“As has been the case in recent times, in 2024 a lot of the international insured losses have been pushed by secondary perils, particularly extreme convective storms within the US,” Swiss Re stated, noting, that the lethal fires in Los Angeles in January this yr level to a different yr of excessive losses from secondary perils.

International financial losses from catastrophes have been US$318 billion, the best since 2017 (US$448 billion in 2024 costs). “Round 43% have been lined by insurance coverage, highlighting the continued existence of huge safety gaps in lots of elements of the world, together with in superior economies,” the report stated. The 2024 insurance coverage safety hole of $181 billion — up from $177 billion in 2023 — is the distinction between general financial losses and insured losses.

Peak-Loss Years

Regardless of the excessive price ticket from secondary perils, Swiss Re warned, it’s major perils (tropical cyclones and earthquakes) that stay the most important contributor to insured losses general. Swiss Re pointed to the 5 so-called “peak loss” years which have occurred within the final 30 years (1999, 2004, 2005, 2011 and 2017), when annual losses have been method above pattern.

In 2017 – the final peak-loss yr – Hurricanes Harvey, Irma and Maria drove international insurance coverage losses to 111% above pattern, however Swiss Re warned that the next interval of quiet since then didn’t sluggish the underlying development of danger.

Swiss Re’s pure disaster fashions level to a 1-in-10 chance that international insured losses may attain as excessive as US$300 billion in 2025, creating subsequent peak-loss yr. (See above graphic).

Swiss Re cautioned that peak loss years, “as a consequence of both the buildup of many loss occasions or these from a number of particular person giant occasions, shouldn’t be thought-about a freak prevalence.” “Historical past repeats, and it’s not a query of if, however when the insurance coverage business will face the following peak loss yr.”

Los Angeles Wildfires

Though 2025 started with file insured wildfire losses of roughly $40 billion in Los Angeles, Swiss Re defined that the fires on their very own won’t trigger a notable deviation from the annual loss development pattern for pure catastrophes (of 5%-7%).

“Of the entire losses, insurance coverage claims for residential property have been a minimum of US$30 billion,” stated Swiss Re, estimating this can doubtless generate a loss ratio of round 200% for owners’ insurers in California.

“Assuming an round 50% base load, the loss ratio is heading in the direction of 250%. The final time the loss ratio was of comparable magnitude was in 2017 (201%) and 2018 (176%), when wildfires in California triggered file losses for that point,” the report added.

“We estimate that two-thirds of payouts to cowl the fireplace losses will come from major insurers, one-third to be paid by reinsurers. The dimensions of losses was so giant that many extra of loss reinsurance covers have been triggered. The reinsurance share of loss would have elevated additional with an excellent greater loss.”

In years that losses are near pattern, Swiss Re stated, major insurers cowl nearly all of property claims, however when main disasters strike and losses rise effectively above pattern, “reinsurers step in to cowl greater than half of the losses in extra of pattern.”

Householders Insurance coverage

Householders in catastrophe-prone states are feeling the ache of rising premiums, as their insurers search to return to underwriting profitability.

Within the US, owners’ insurers have seen their internet incurred losses improve by 8% yearly since 2018 – a pattern pushed by a post-COVID surge in development and claims prices. “The consequence of the latter is that house owner insurers have seen a number of years of underwriting losses,” Swiss Re stated.

“After a number of years of underwriting losses, owners’ premiums solely not too long ago caught up with housing alternative prices. Nonetheless, ongoing underwriting losses counsel that premiums are nonetheless not commensurate with the chance, and that additional alignment is important to maintain insurance coverage enterprise.”

The states with highest exposures to pure catastrophes are additionally these the place, normally, house owner premiums are highest, the report stated, pointing to 5 states – Florida, Texas, California, Louisiana and Colorado – which account for round 50% of all pure disaster losses within the U.S.

“Traditionally, Louisiana has suffered the best pure disaster losses per coverage, adopted by Florida. These have principally been on account of losses emanating from hurricane occasions,” the report confirmed.

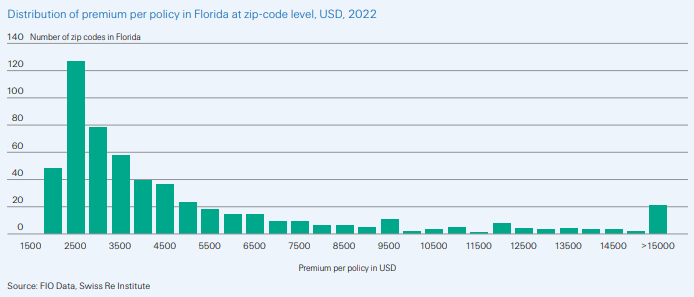

“Home-owner premiums per family within the state of Florida are twice the nationwide common,” the report stated, noting that in states with increased common premiums (equivalent to Florida), extraordinarily excessive premium ranges are localized.

For instance, in 11% of the Florida’s zip codes, premiums per coverage have been above US$10,000, the report stated. “These are sometimes coastal zip codes with highest danger of storm surge and/or wind injury.”

{Photograph}: A home lies toppled off its stilts after the passage of Hurricane Milton, in Bradenton Seashore on Anna Maria Island, Fla., Oct. 10, 2024. (AP Picture/Rebecca Blackwell, File)

Associated:

Matters

Trends

Profit Loss

Claims

{kind=link}